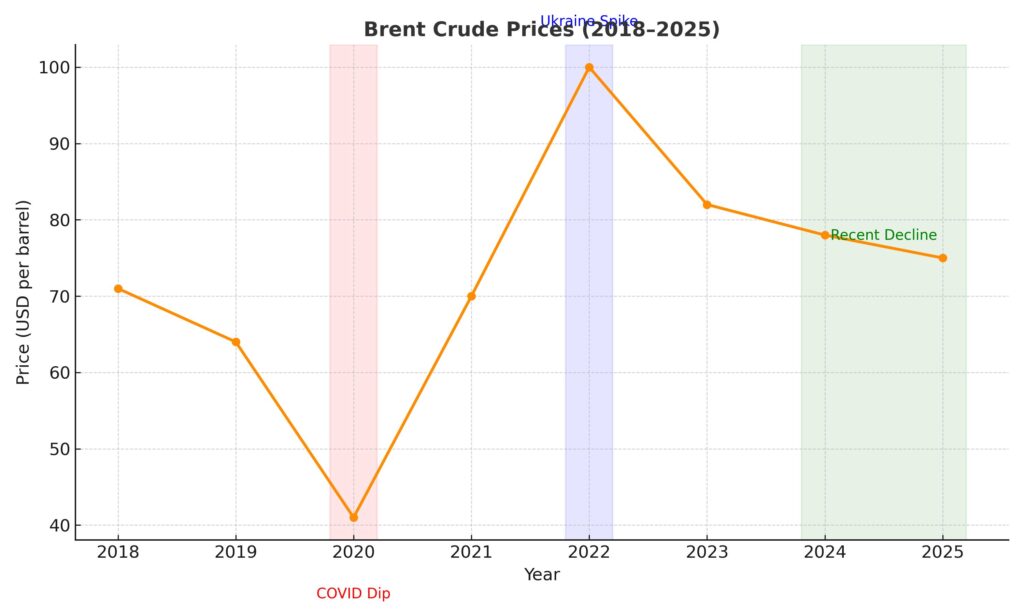

Oil prices are on edge. In early October 2025, Brent crude edged around $66–67/barrel, while U.S. WTI hovered near $62–63. These levels mark a soft pullback from recent highs, and they come amid growing ambiguity over OPEC+ production strategy, rising non-OPEC output, and worries over global demand.

To many analysts, this is not a mere blip it’s a signal that the delicate balance between supply and demand is tilting. In this article, we unpack the forces driving the fall, assess the broader consequences, and explore regional angles that matter to India, the Gulf, and emerging markets.

What’s Driving the Dip?

1. OPEC+ Supply Uncertainty

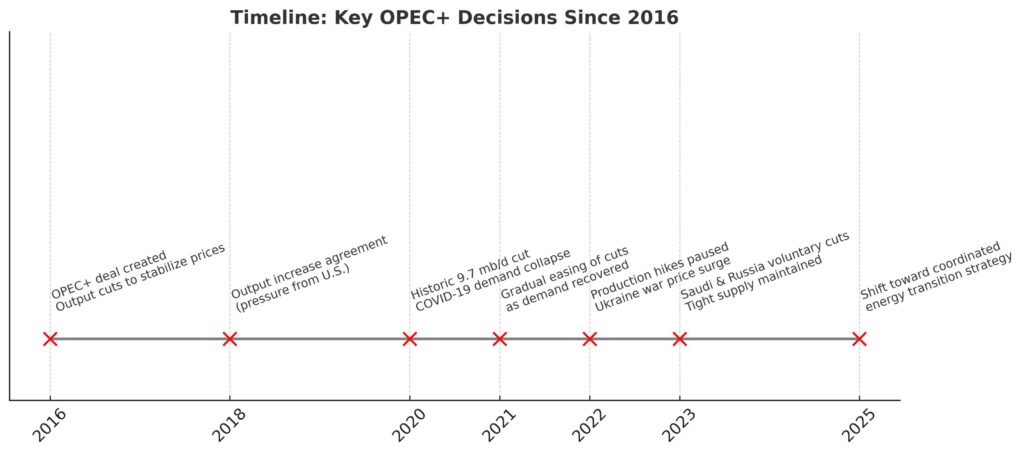

Perhaps the most consequential factor is the shifting stance of OPEC+. After a protracted period of production cuts, the alliance has gradually moved toward unwinding those cuts. In recent weeks:

- Reports suggested OPEC+ may raise output in November by 137,000 barrels per day (bpd).

- The Joint Ministerial Monitoring Committee (JMMC) stressed compliance but admitted that many members have been missing quotas.

- Actual output has fallen short: in recent months, OPEC+ has delivered only ~75% of promised increases, largely due to capacity constraints among smaller producers.

These signals inject uncertainty about how aggressive production increases will be and thus how much downside pressure they will exert.

2. Rising Non-OPEC Output & Inventory Pressure

While OPEC+ debates, non-OPEC producers like the U.S., Brazil, Guyana, and Canada continue expanding output. Analysts expect non-OPEC supply to grow by ~1.0 million bpd in 2025, contributing to surplus risk.

Concurrently, the EIA’s Short-Term Energy Outlook forecasts that global oil inventories will build by over 2 million bpd in late 2025–early 2026, driving Brent prices down toward $59/barrel in Q4.

3. Weakening Demand Sentiment

Global demand is showing strains. Key economies like China and Europe are flirting with slowdowns. In the U.S., recession fears and tariff pressures weigh on consumption and industrial activity. Markets are reading these signals:

- A Reuters poll of 32 analysts projects Brent will average $67.61 for 2025, slightly below earlier forecasts. Reuters

- The U.S. Energy Information Administration (EIA) warns of “higher volatility” as OPEC+ output increases and trade uncertainty suppresses demand confidence.

- A recent build in U.S. oil and fuel inventories (especially in gasoline & distillates) dampens near-term fuel demand prospects.

Thus, even as supply threatens to surge, demand is looking softer a classic recipe for price consolidation.

Regional & Local Angles: Why This Matters for India, the Gulf & Beyond

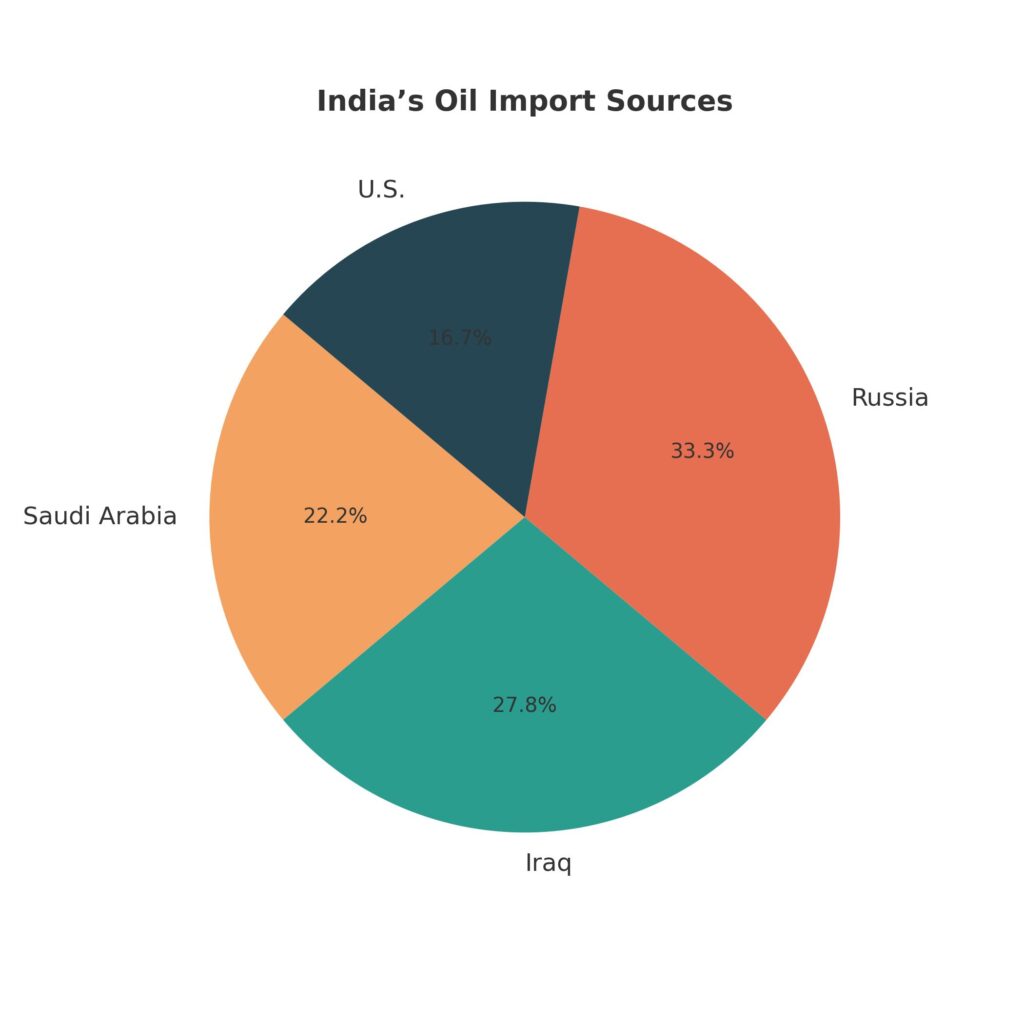

India: Importer Vexation

India imports roughly 80% of its oil needs. A fall in global prices offers short-term relief in import bills but carries risks:

- Fiscal stress relief: Lower crude prices ease subsidy burdens and free up budget space.

- Refinery margins squeeze: Indian refiners, many geared for higher global benchmarks, may see margins shrink.

- Energy mix decisions: Cheaper oil may weaken urgency for renewables, complicating India’s carbon transition goals.

If prices dive further toward $55–60, India could enjoy relief but such drops may also reflect deeper global weakness, which could hurt Indian exports and capital inflows.

Gulf & OPEC Exporters: Balancing Act

For Gulf producers, lower prices spell direct fiscal pain. While they argue for preserving market share, they also guard revenue stability.

- Saudi Arabia and UAE hold spare capacity and may use output as a tool to discipline members.

- But sustained soft prices could force Gulf states to cut spending or dip into reserves reducing their ability to sustain influence in regional geopolitics.

The tariff-driven instability (e.g., U.S. foreign policy, sanctions) also raises the importance of non-dollar inflows, making rupee or other regional settlement mechanisms more attractive.

Geopolitics: Russia, U.S., and Beyond

- Russia remains a key swing producer. Recent drone strikes on its refineries and an export ban on diesel/gasoline underscore volatility risk.

- The looming U.S. government shutdown threatens to delay energy data and complicate market confidence.

- Meanwhile, trade tariffs, especially by the U.S., raise fears of a global slowdown which would pull down oil demand further.

In this web, oil isn’t just a commodity it’s a geopolitical lever.

Historical Comparisons & Lessons

- 1979 Oil Crisis: The Iranian Revolution triggered supply shock, prices doubled within months. The lesson: supply disruption can shatter price norms.

- 2020 Russia–Saudi Price War: Amid COVID demand collapse, OPEC+ broke down and flooded markets with supply prices collapsed below $20.

- Today’s situation differs: slowdown is demand-led; OPEC+ capacity is constrained. But if misjudged, similar overshoot could follow.

Furthermore, the shift of non-OPEC supply dominance is reminiscent of past periods when OPEC lost pricing power increasing the odds that output competition, not cartel discipline, will define market cycles.

Scenarios: Where Oil Could Go from Here

| Scenario | Probability | Price Outcome | Key Drivers |

|---|---|---|---|

| Soft Landing / Balanced | Medium | Brent $65–70 | OPEC moderates output, demand steadies |

| Supply Surge / Demand Weakness | High | Brent ↓ to $55–60 | Non-OPEC oversupply + demand slowdown |

| Geopolitical Disruption | Low-Medium | Brent spike >$80 | Wars, pipeline attacks, sanctions |

| OPEC Reversion | Low | Brent rebounds to $75+ | Deep cuts restore balance & confidence |

A key wildcard: whether OPEC+ can hold discipline and match output to realistic demand growth.

My Take: Why This Dip Might Be More Than a Pullback

While many see a dip as profit-taking or short-term sentiment, I believe we’re witnessing the onset of a structural shift in oil markets.

- Cartel fatigue: OPEC+ is showing signs of internal fractures. Quota misses and varying incentive alignment weaken authority.

- Rise of independents: Non-OPEC players are no longer followers they shape fundamentals.

- Demand rethinking: As global economies pivot to efficiency, renewables and energy efficiency could trim long-term oil demand growth.

- Currency & financing vectors: In a world of dollar pressure, markets may price in financing stress, not just physical oil flow.

If oil stays weak, we may enter a world where supply discipline pays off only if matched by credible demand growth and where energy geopolitics becomes more fragmented.

What to Watch (Short-Term Indicators)

- OPEC+ meeting outcomes (especially November quota decisions).

- U.S. crude inventory data (API, EIA).

- Russian export disruptions (sanctions, refinery damage).

- Global macro health: China PMI, U.S. durable goods, European inflation.

- FX & bond markets weak oil could spur dollar strength, pressuring emerging markets.

Conclusion: Soft Slide or Structural Shift?

In conventional cycles, a soft pullback amid OPEC uncertainty is expected. But today’s mix rising base supply, contested cartel dynamics, volatile demand, and geopolitical stress suggests this might mark a deeper inflection in oil markets.

For India, lower oil means breathing room for the fiscal budget but also warning signs for export demand. For Gulf producers, it’s a test of resilience. And for global markets, it may herald a future where oil is no longer the uncontested king of commodities.

We’re watching not just a price drop but possibly the unraveling seams of the old oil order.

Abhi Platia is a financial analyst and geopolitical columnist who writes on global trade, central banks, and energy markets. At GeoEconomic Times, he focuses on making complex economic and geopolitical shifts clear and relevant for readers, with insights connecting global events to India, Asia, and emerging markets.